BooHoo Shares Forecast January 2022 – Time to Buy BOO?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

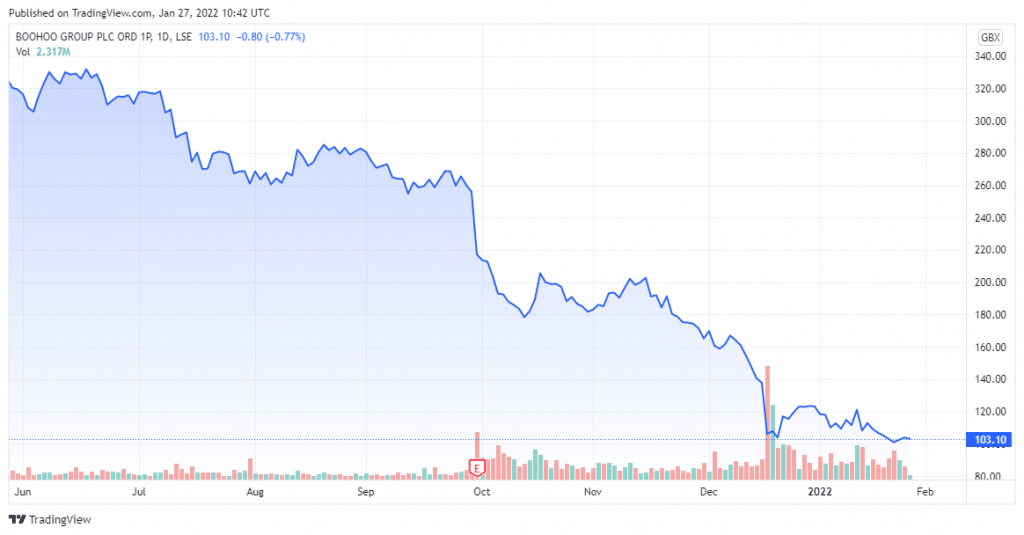

Shares of online fashion retailer BooHoo are in the green today, after closing at £103.90 as of January 27th (08:02 GMT). BOO shares have had an awful 12 months which made it the second-worst performer in the FTSE AIM 100 index over this time period. They have crashed by 71% as they have tackled a number of issues related to the pandemic. With revenue growth slowing and costs increasing, it doesn’t look good for the company ahead.

BooHoo – Technical Analysis

The financial statement indicated by BooHoo indicates a market cap of £1.247 billion with total assets worth £942.7 million. The revenue for 2020 was at £1.75 billion with a profit margin of 5.20% compared to £1.23 billion in 2019.

Moving averages such as Exponential Moving Average (10)(105.54), Simple Moving Average (10)( 105.40), Exponential Moving Average (20)(111.58), Simple Moving Average (20)(110.83) and Exponential Moving Average (30)(119.04) are giving a sell indication. Oscillators such as Relative Strength Index (14)(34.73), Stochastic %K (14, 3, 3)(20.73), Commodity Channel Index (20)(−109.05), Average Directional Index (14)(43.60) and Awesome Oscillator(−17.56) are neutral.

68% of all retail investor accounts lose money when trading CFDs with this provider.

Recent Developments

For Boohoo, growth has stalled in fiscal year 2022 (the 12 months to 28 February 2022). The company has gobbled up some of its competitors due to the failure of brands such as Topshop and Warehouse. This provided BooHoo with the opportunity to buy these brands at knockdown prices, vastly expanding its range and reinforcing its position in the UK retail market. Boohoo is well-positioned to adapt to the booming e-commerce market, as rivals have struggled.

However, Boohoo has less financial room to manoeuvre as it sells clothes at very cheap prices. This means that it is less efficient when it comes to absorbing cost inflation. It has also been criticized for some of its labour practices in the past. Reputational risks will continue to remain so long as the business focuses on very cheap clothes. However, if it damages the consumer appeal of Boohoo, both sales and profits could go down. Boohoo has taken some steps to improve labour conditions in its supply chain.

Should You Buy BOO Shares?

Boohoo has had its revenue cut from between 20% to 25% to the now lower 12% to 14%. The share price will not surge from here if it becomes a slower-growing business. Boohoo has experienced significantly higher returns This could very well be due to Omicron where festive party celebrations were cancelled, leading to the increased return rates. Costs have also been affected by ongoing supply chain issues as the pandemic has impacted delivery times and increased freight costs. However, these are mainly transient risks.

Some analysts have also questioned Boohoo’s past deals and whether or not they represented the best outcome for investors. Boohoo’s bottom line is currently under pressure from rising costs and increasing volume of order returns. These are the challenges Boohoo has had to deal with over the past couple of years. Concentrating on these issues alone, some investors might be avoiding the shares.

This is an excellent opportunity to buy BOO shares. With a cash-rich balance sheet history of integrating acquisitions and current valuation, the company has done well over the past couple of years. Concentrating on these issues alone, I can see why some investors might be avoiding the business. But there is plenty of upside remaining.

Buy BOO Stock at eToro from just $50 Now!