DocuSign Share Forecast January 2022 – Time to Buy DOCU?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

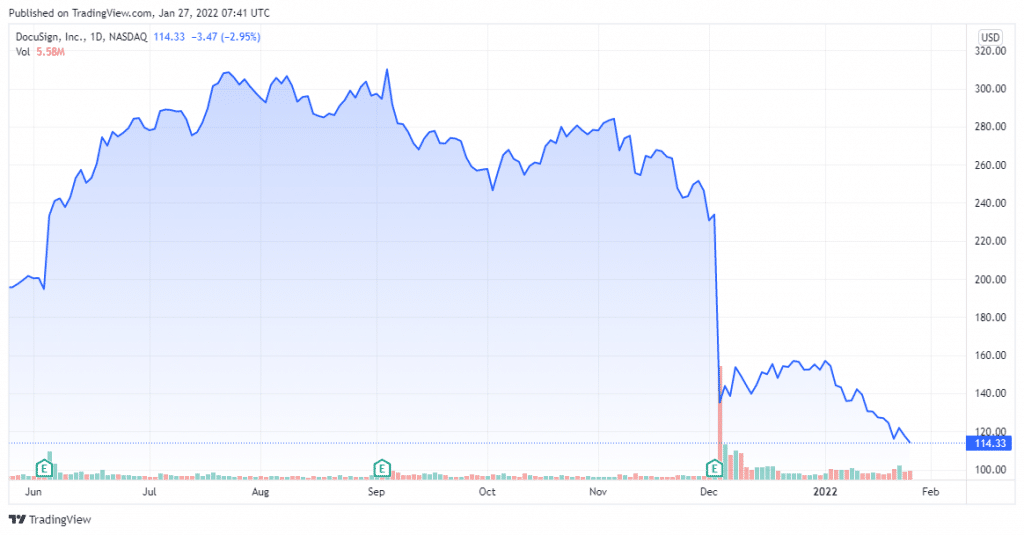

Shares of DocuSign (NASDAQ: DOCU) are in the red today after closing at $114.33 as of January 26th (19:59 EST). Investors got scared last year due to DocuSign’s share price volatility. DOCU shares are trading at their lowest forward-price-to-sales ratio since the spring of 2020. DOCU ended down 51% from its peak.

DocuSign – Technical Analysis

The financial statement released by DocuSign indicates a market cap of $22.623 billion with total assets worth $2.411 billion. Revenue for 2020 was at $1.45 billion with a profit margin of -16.74% compared to $973.97 million in 2019.

Oscillators such as Relative Strength Index (14)(26.89), Stochastic %K (14, 3, 3)(22.00), Commodity Channel Index (20)(−125.95), Average Directional Index (14)(41.44) and Awesome Oscillator(−22.40) are neutral. Moving averages such as Exponential Moving Average (10)(124.55), Simple Moving Average (10)(124.91), Exponential Moving Average (20)(134.54), Simple Moving Average (20)(136.10) and Exponential Moving Average (30)(145.42) are indicating a sell action.

68% of all retail investor accounts lose money when trading CFDs with this provider.

Recent Developments

DocuSign is known as a company that helps its clients create official digital signatures for documents. The Corona pandemic was a huge tailwind for the company. The company was on a steady growth path well before the pandemic arrived on the scene. DocuSign’s fiscal 2021 Q3 revenue was 42%. Since the beginning of 2019, the company has produced year-over-year revenue growth of between 37% and 58%. Its gross margin is 79% compared to 74% in the year-ago quarter. Net loss for DocuSign decreased from $58 million in fiscal Q3 2021 to a loss of $6 million in fiscal Q3 2022. It’s safe to say that the company’s top and bottom lines have been steadily growing over the last 2 years.

Compared to the 820,000 at the end of the prior-year period, DocuSign grew that number to 1.1 million customers at the end of fiscal Q3. It represented a 45% increase in the number of enterprise and commercial customers. However, investors reacted negatively to this news as it was paired up with a deceleration in growth compared to recent quarters. This was expected as some of its growth was pulled forward as customers adopted DocuSign’s services out of necessity. Customer growth is still ahead of its pre-pandemic pace.

Should You Buy DOCU Shares?

Investors have a lot of reasons to invest in DocuSign, one of which is its Agreement Cloud software. It is a product for automating and connecting an entire agreement process. It can save several hours of work by implementing AI. This allows the software to search agreements for specific language or clauses, highlighting the more important aspects, and reducing the time and expense. It is definitely a revenue driver for the company.

However, investors interested in DOCU also have to consider a few risks. The company’s revenue and customer growth rates have slowed sequentially over the last few quarters. Investors will thus be checking whether the same trend continues when the company reports earnings again. They should wait and see before the valuation rebounds.

That being said, DocuSign is still a good company to invest in, and at current levels, it is an attractive buying opportunity. Currently, DOCU shares are trading for only 11 times forward sales, a low it hadn’t touched since the spring of 2020. The company does not carry the risk of stretched valuation anymore. This is poised to work in the investor’s favour. Considering this now is a good time to add DOCU shares to your portfolio.

Buy DOCU Stock at eToro from just $50 Now!