Markets Cautious Ahead of Central Bank Decisions, Omicron Concerns

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

Global markets will be dominated by the outcome of central bank meetings, including the Fed, ECB and BoE, and the latest news on the omicron variant of the Covid virus.

Altogether there are 20 central bank meetings, with the US Fed, the European Central Bank and the Bank of England all set to make decisions on interest rates.

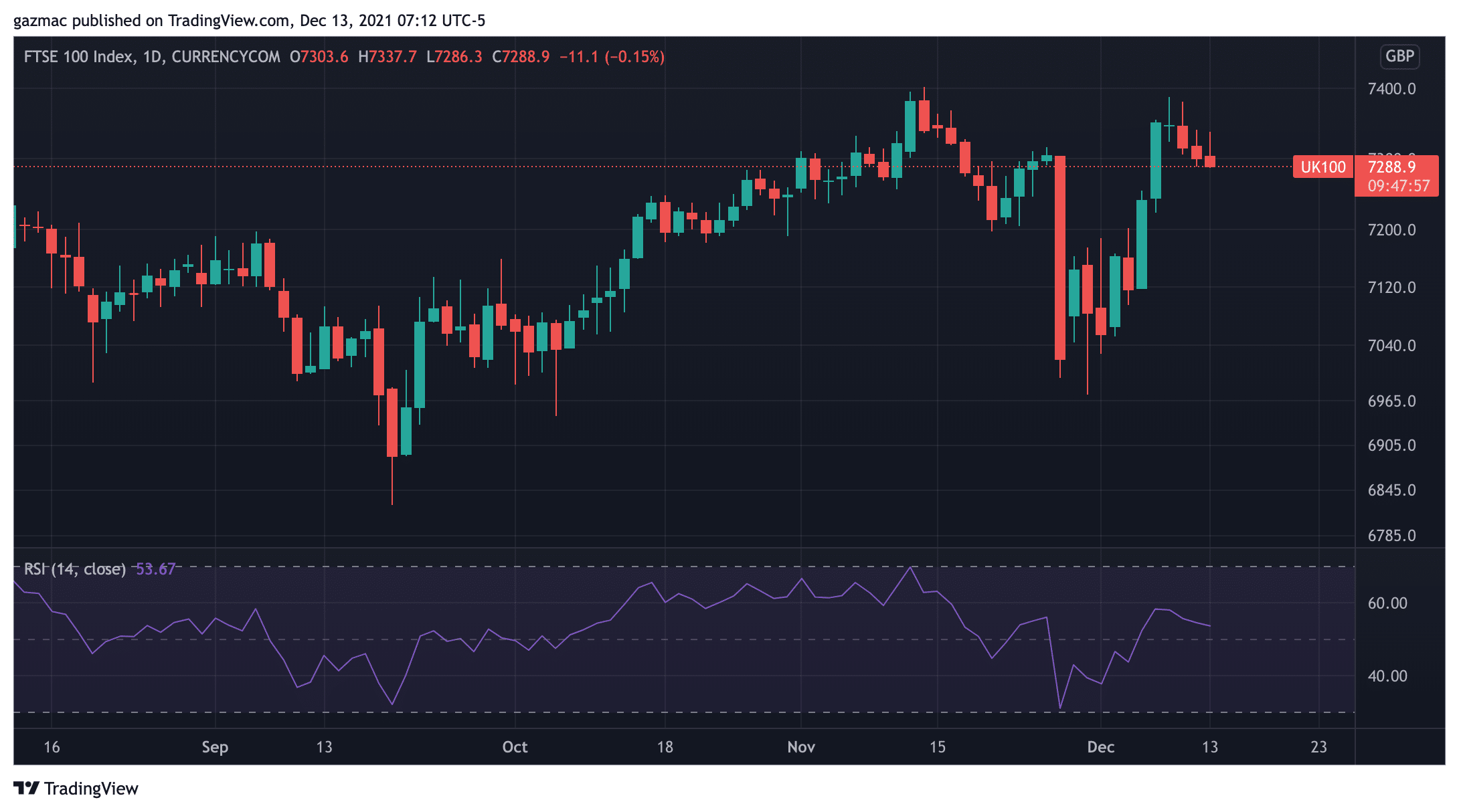

European equity markets started the session trading higher, with the exception of the FTSE 100 as traders reacts adversely to the government’s decision yesterday to raise its threat level for the Covid pandemic from 3 to 4, with 5 being the highest level.

UK prime minister Boris Johnson announced on Sunday that the country was facing an emergency from a “tidal wave” of infections due to the omicron variant and would therefore be accelerating rollout of booster vaccines.

The health secretary refused to rule out the possibility of school closures, which could have a major negative impact on the economy. New work from home guidance comes into effect on Wednesday.

Stocks start week tentatively higher

The Euro Stoxx 50 index is up 0.87% higher, while Germany’s Dax is up 1% at 15,778, while the FTSE 100 began in the red but was doing its best to stay positive by mid morning. In Asian markets Japan’s Nikkei was 0.7% higher and Hong Kong’s Hang Seng index finished in the red , down 0.2%.

US futures were all trading higher, with the S&P 500 0.3% higher as the markets look set to build on last week’s record highs. Even though inflation came in at 6.8%, that was in line with forecasts

Positive noises from China’s policymakers concerning the possibility of accommodative expansionist policies have helped commodity prices, with iron ore and copper major beneficiaries, but crude oil benchmarks are around 0.4% lower.

Market participants will be attentive to what the Fed decides to do on tapering. Expectations are for the plan to end the tapering by the end of May next year to be speeded up, so that purchases come to an end in February.

Central banks caught between falling behind curve and overreaction

The Fed is under pressure to move more quickly to run down asset purchases because of the elevated US inflation reading in the country, which reached a 39-year high of 6.8% last week.

ING analysts support the view of pressure to rein back stimulus, which would still be substantial even after tapering ends:

“Even with the end of QE buying, the Fed’s policy stance will remain highly stimulative and in an environment of strong growth, decent jobs momentum and elevated inflation pressures, the case for withdrawing some of the stimuli, appears strong.”

Similarly, the European Central Bank is also facing pressure to act to reduce its stimulus programme and asset purchases. But like Fed policymakers, the ECB policymakers will be concerned that they may end up overreacting on inflation if omicron leads to measures that negatively impact on economic activity, which in turn could help to temper inflation rates.

The Bank of England was thought likely to raise interest rates before the end of the year but the emergence of the omicron virus has changed the thinking on that. Traders are taking their bets off the table for a tightening in policy with a rate rise now seen as less likely.

Although inflation is high, the omicron virus could force the UK government to reintroduce measures to curb the spread of the pandemic, thereby dampening economic activity.

Data from South Africa appears to confirm that the Covid disease symptoms are milder with omicron, but the young demographic of the South African population and other factors mean that epidemiologists cannot be certain.

Central bank decisions: FOMC, BoE, ECB economic calendar dates

UK employment data is on tap on Tuesday, with economists expecting employment to add 224,000 jobs in September compared to 247k the previous month. Unemployment should fall from 4.3% to 4.2%.

On Wednesday the Federal Open Market Committee (FOMC) ends its two-day meeting with an announcement on interest rates and tapering. Its press conference will begin at 19:30 GMT. Rates will remain unchanged at 0.25%, but it will be action around tapering and comments at the press conference that will be closely watched for indications as to when the first rate decision might be taken in 2022.

Other economic news coming out of the US includes the retail sales figures which are expected to grow 0.8% in November compared to 1.7% in the previous month.

Canadian inflation data is out Wednesday, with the headline figure expected to remain unchanged at 4.7%, although core will fall from 3.8% to 3.6%.

In the UK, inflation is forecast to continue its upward trajectory, up from 4.2% in October to 4.7% in November, year on year.

On Thursday 16th the European Central Bank and the Bank of England both makes their interest rate decisions.