HSBC Shares Higher on 3Q Earnings Surprise, Rate Hike to Boost Profits

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

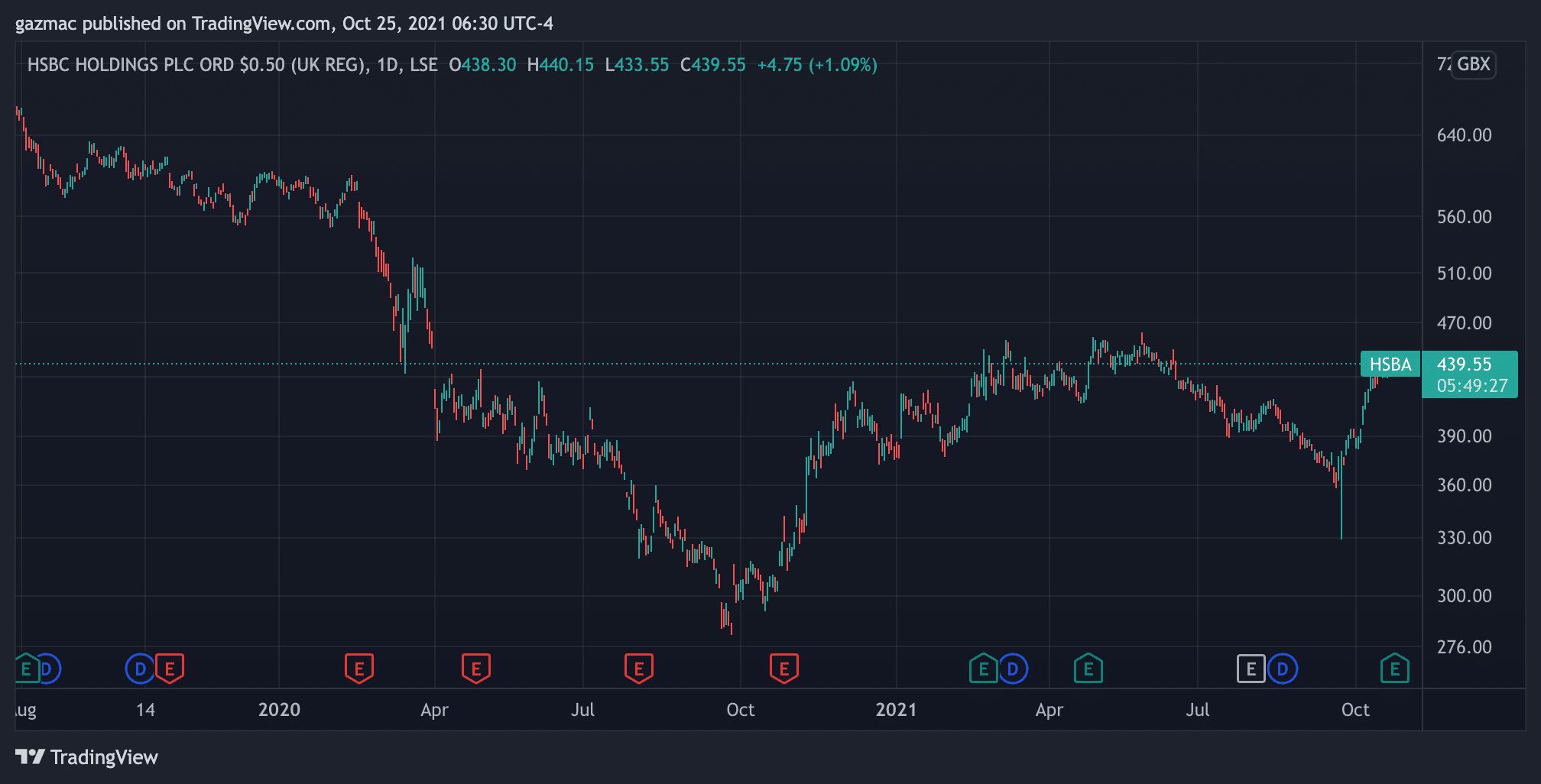

HSBC (HSBA) shares are trading higher today, with the rebounding world economy leading to a 74% surge in profits at the global banking group.

The bank has announced a $2 billion share buyback which saw the share price rise has jumped 1% in early London trade, although the price shares have pared some of those gains. HSBC shares are currently priced at 439p.

Pre-tax profits for the quarter to September rose to $5.4 billion compared to $3.1 billion the previous year, handsomely beating analyst HSBC forecasts of $3.8 billion.

Profits were boosted the release of expected credit losses “and other impairment charges and a higher share of profit from our associates”, the statement read.

Bad debt provision reduced by $659 million

Bad debt provision has been reduced by $659 million after it had increased provision a year earlier by $823 million.

Investors had been worried that HSBC may have seen its results hurt by the troubles in the Chinese property market but on this evidence there don’t appear to be any issues there for the bank as yet.

However, HSBC said costs would rise more than previously projected, by $1 billion to $32 billion, with the bank blaming inflationary pressures.

“We continued to demonstrate strong cost control over the course of the year. Given inflationary pressures, continued investment and the impact and timing of recently announced acquisitions and disposals, we now expect adjusted costs of approximately $32 billion for 2021 and 2022, excluding the estimated UK bank levy charge of $300 million.”

“With an improved revenue outlook and the prospect of rising policy rates, we remain committed to achieving a RoTE of greater than or equal to 10% over the medium term,” the earnings release statement noted.

RoTE – return on tangible equity – is a measure of profitability and in the banking sector a reading of 10% is considered to be respectable.

“Lows of recent quarter behind us” says CEO Quinn

Chief executive Noel Quinn in comments accompanying the results announcement, wrote: “We had a good third-quarter performance, with strong growth in profits supported by additional credit provision releases. Our strategy remains on track, with good delivery in all areas. This was reflected in more consistent top-line growth, robust lending pipelines across our businesses, and rising trade and mortgage balances.”

“While we retain a cautious outlook on the external risk environment, we believe that the lows of recent quarters are behind us. This confidence, together with our strong capital position, enables us to announce a share buyback of up to $2 billion, which we expect to commence shortly,” he added.

Investors will be cheered by the bounce-back in performance, which last year saw profits fall back 45% as a result of the pandemic sucking demand out of the world economy, not helped by continuing low interest rates.

The bank’s performance has been a marked improvement on 2020, when profits fell 45 per cent as banks were hit by ultra-low rates, a slowdown in trade and the fallout from global lockdowns.

HSBC 3Q interim dividend payment of 7 cents

Dividend per share is $0.22 for the year ending 31 December 2021, which includes an interim payment of 7 cents paid in September.

The interim dividend was able to be paid to shareholders following the removal by the Bank of England of restrictions as the recovery from the pandemic gathered pace, which the central bank decided that bank stocks were in a strong enough financial position to warrant the resumption of payouts to shareholders.

HSBC is a favourite with Hong Kong retail investors and other Asian investors. Of the 17.9 billion in adjusted pre-tax profits in the first three quarters of the year, $10.4 billion came from its Asia business.

HSBC shares: double-down on Asia growth paying off?

The bank has made a strategic shift to double-down on its Asian roots with a strategic “pivot to Asia”. That seems to be paying off with strong trading activity in Hong Kong and Shanghai exchanges due to the heightened volatility in equities and also strong business in wealth management.

Adjusted revenue in its wealth management segment was $6.98 billion in the nine months to September, compared to $5.88 in the same period last year, although lower on a quarterly view.

But revenue was 11% lower in personal banking, down $1.1 billion to $9.2 billion. Net interest income was down by 1% due to lower global interest rates.

Asset management revenue was also higher, up 15%. However, this was from a small footprint in that sector, bringing in a mere $100 million, which is also partly a reflection of the fee compression that continues to hurt margins in the fund management industry as the proportion of lower fee passive vehicle proliferates in the form of exchange-traded funds.

In 2020 the bank merged its wealth management and retail banking divisions, renaming them in the process as Wealth and Personal Banking, respectively. It also acquired insurance giant Axa’s Singapore wealth management subsidiary in August.

Forthcoming interest rate hikes “kicker” for HSBC shares performance says CFO

With interest rates expected to start rising in the major economies as soon as the end of this year and early in 2021, the bank is bullish in its trading forecast.

Chief Financial Officer Ewen Stevenson said: “We do think that we are close to an inflection point now in revenues. If we do get rate rises it will be a very material kicker to our performance.”

Stevenson told Bloomberg TV that the bank does note expect to be affected by Evergrande’s debt problems.

The bank’s key CET1 ratio, which is a measure of capital to assets, of which at least 6% must be tier 1 capital, according to the Basle Accords, was 15.9% as at 30 September 2021, up from 15.6% on 30 June 2021.

Another measure of financial health – its liquidity coverage ratio, the proportion of high liquid asset to meet short-term obligation – was also good at 135%.