Australian regulators hint to upcoming crackdown of home loans

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

Australian regulators appear to be ready to implement some measures that aim to curve the rate at which home prices are soaring in the country as indicated by the latest comments from the country’s Treasurer, Josh Frydenberg.

According to a statement from the country’s finance minister following a meeting with regulators in which the current conditions of the real estate market were discussed, the economy seems “well positioned to recover as restrictions ease” and this strength should serve as the appropriate setup to implement macroprudential policies to take some pressure off prices.

The Treasurer further stated that these measures aim to prevent instability in the real estate market amid a worrying increase in the volume of bad credit loans and investment-focused lending.

According to data from the Australian Bureau of Statistics, the volume of new home loan commitments – excluding refinancing – has almost doubled since its post-pandemic low of $16.66 billion in May 2020 to $32.12 billion by the end of July.

Meanwhile, loans taken for investment purposes have climbed near their 2015 high of $10 billion indicating that some speculative activity could be contributing to pushing prices higher in the current low interest rate environment.

Low interest rates prompt buyers to invest

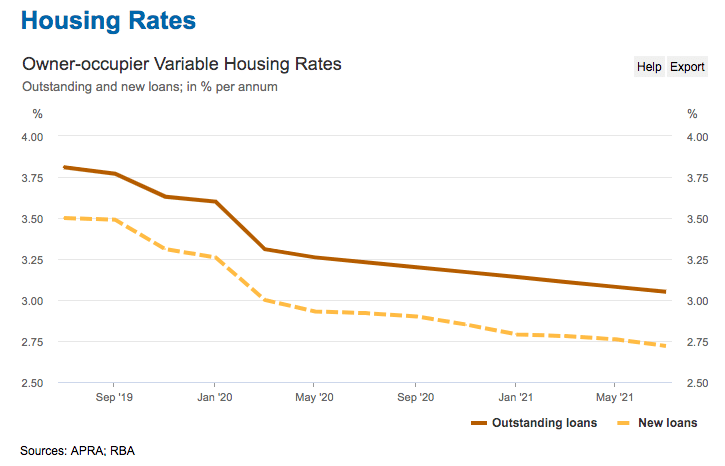

Data from the Reserve Bank of Australia shows the extent of the decline that housing rates have experienced amid the expansionary monetary policies the central bank adopted during the virus crisis, with the average rate assigned to new loans currently standing at around 2.7%.

For owner-occupied home loans, new loans can get approved at a rate as low as 2.32% per year while for investment-focused operations the rate for new loans is dramatically low as well at 2.74%.

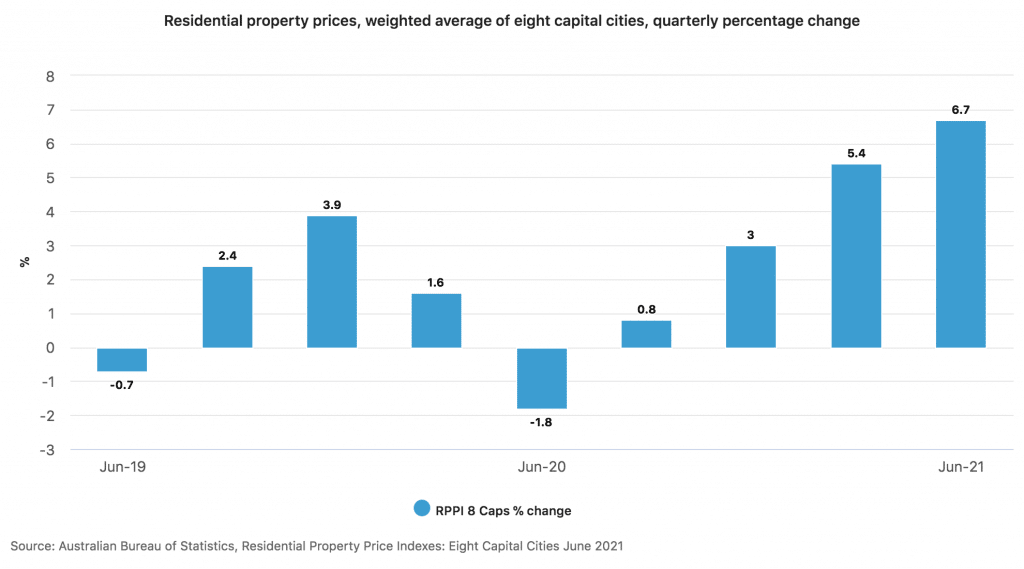

This favorable environment has pushed the average home price in the country’s top eight capital cities by 16.8% during the twelve months ended in June while the 12-month advance in certain cities like Sidney, Canberra, and Hobart has exceeded that figure.

For authorities, an overheated housing market could lead to an increase in systemic risks as borrowers might feel too comfortable taking more than debt than they can afford, especially for investment operations.

Which policies could be implemented to alleviate the pressure?

Curving the advance of the housing market is now becoming a crucial target for the Council of Financial Regulators as the topic has already been discussed in its latest meeting.

Among the measures that could be implemented to protect the financial system, the Australian Prudential Regulation Authority (APRA), the country’s top banking regulator, could impose a cap on the percentage of the home loan portfolio that can be directed to investment-focused loans.

Moreover, other measures could seek to demand a higher buffer from prospective borrowers. This rule will seek to reduce the risk of default if interest rates increase.

Additionally, interest-only loans, which are considered riskier amid their higher loan-to-value ratio and the potential losses they could cause to banks if property prices decline sharply, may also be limited to the extent that they account for a relatively small percentage of a lender’s total home loan portfolio.

How could these macroprudential policies affect home prices?

In a report released in early September this year, CoreLogic, a research firm that specializes in the Australian real estate market, highlighted that policy changes could lead to a rapid and sharp correction in home prices in the country, similar to what has happened in the past.

Citing previous rounds of macroprudential policy changes, CoreLogic emphasized that a tightening in credit conditions by the Reserve Bank of Australia (RBA) could result in lower house prices in subsequent years, especially in cities that are a common target for investors.

All things considered, a move from regulators at this point seems prudent upon considering the percentage of loans that are being issued to borrowers with elevated debt-to-income ratios – an indication that the currently favorable conditions are prompting banks to take on more risks than they should when lending.