Lloyds Banking Group Share Price Forecast August 2021 – Time to Buy LLOY?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

Shares of Britain-based Lloyds Banking Group (LSE: LLOY) are in the green today, currently trading around the 49p range. LLOY shares have experienced a 53% rise over the last 12 months. However, this is bleak in comparison with rivals Natwest Group, which gained 87% and Barclays which has gained 63%. While it’s offering a 5% dividend yield, is it enough to reason to buy these shares? Let’s find out.

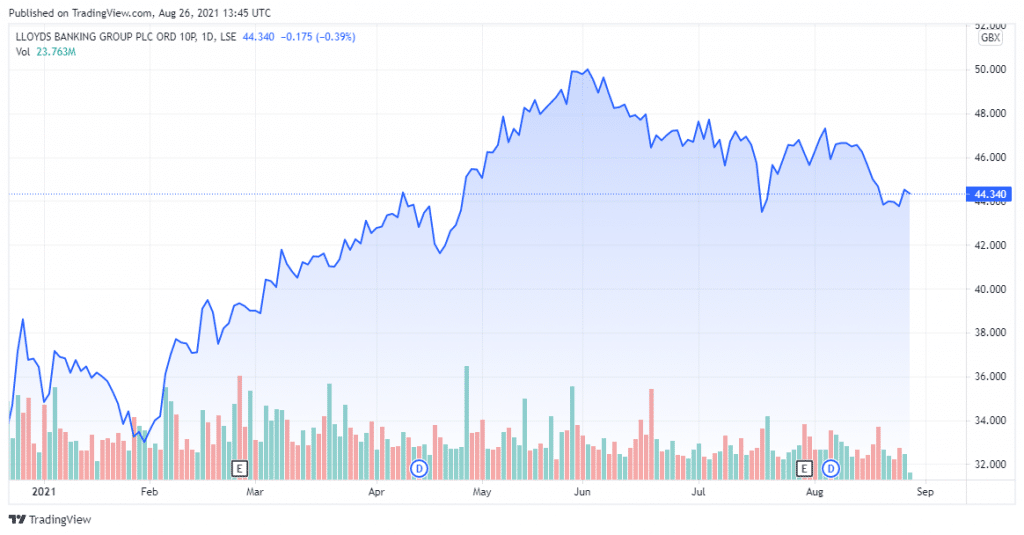

Lloyds Banking Group – Technical Analysis

According to Lloyds Banking Group’s financial statement, the company’s market cap is at £31.187 billion and total assets worth £879.687 billion. The revenue for 2020 was at £34.12 billion compared to £49.42 billion the year before.

Moving averages for Lloyds Banking Group such as Exponential Moving Average (50)(45.826), Simple Moving Average (50)(46.135), Exponential Moving Average (100)(45.031) and Simple Moving Average (100)(46.259) are pointing towards a selling action. Oscillators such as Stochastic RSI Fast (3, 3, 14, 14)(9.970), Williams Percent Range (14)(−73.014), Bull Bear Power(−1.812) and Ultimate Oscillator (7, 14, 28)(46.81) are neutral.

67% of all retail investor accounts lose money when trading CFDs with this provider.

Recent Developments

Lloyds has become of the biggest providers of everyday banking as well as the biggest mortgage lender in the United Kingdom with brands such as Halifax and Bank of Scotland under its belt. It is also one of the largest providers of motor finance and leasing via Black Horse and Lex Autolease, the largest provider for credit cards via MBNA as well as retirement products in the United Kingdom. Unlike its rivals, it does not have an investment banking division and does not have operations abroad. All of this makes LLOY shares a pure-play investment in the economy of the United Kingdom, especially the housing market. This is one of the reasons why the share price growth has slowed since May, as the country’s housing sales and mortgage rates have continued to fall.

One of the problems that Lloyds seem to be facing is that it wants to become one of the country’s biggest rental landlords. It has already made moves to enter the build-to-rent market by forming a partnership with FTSE 100 housebuilder Barratt Developments. As part of this arrangement, Lloyds will fund the housing projects and rent them out to increase its return on equity. Given today’s low interest rates, rental properties will produce higher returns compared to financial assets such as government debt. This plan carries significant risk as Lloyds isn’t a very experienced residential landlord as its mortgage lender. It will have to simultaneously build a good reputation with its clientele while keeping costs to a minimum to maintain its high profile business status.

Should You Buy LLOY Shares?

Investors got a fairly flat picture when the bank released its results for the first half of 2021, which showed a decrease in pre-tax profit by 4% from the previous year to reach £3,409 million. While it’s too early to predict how the rest of the year will turn out for the company, various broker forecasts suggest that profits will fall around 20% in 2022 after peaking this year. Because of the sheer size of the bank, various measures to improve profitability such as the build-to-rent scheme will take time before showing results.

Currently, Lloyd’s share price is hovering around the 44p range which is 20% lower than its tangible book value of almost 56p per share. At these levels, LLOY shares are cheap at the moment. But the share price will rise slowly until the group can deliver sustained improvement on profitability. While investors shouldn’t expect any significant gains in September, they can go ahead and pick up these cheap shares for income.

Buy LLOY Stock at eToro from just $50 Now!