Amazon Stock Down 3% in August – Time to Buy AMZN Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

The price of Amazon shares has slipped in August following a pronounced drop in the stock in late July as a result of disappointing third-quarter guidance.

Meanwhile, the performance of the e-commerce giant remains underwater for the year as market participants appear to be expecting a deceleration in the firm’s growth after the remarkable jump that Amazon’s business volumes experienced during the health crisis.

During the second quarter of the year, the company founded by Jeff Bezos reported revenues of $113 billion resulting in a 27% jump compared to the previous year yet the figure missed analysts’ estimates of $115.2 billion for the quarter.

Meanwhile, GAAP earnings per share landed at $15.12 or $2.82 above the Street’s consensus while the number also resulted in a 47% jump compared to the same period a year ago.

Could this downtick result in an opportunity to buy Amazon shares at a lower price or is this slowdown in the firm’s growth rates a sign of an upcoming potential downtrend?

In the following article, I’ll take a closer look at the latest price action while discussing the firm’s fundamentals to draft potential scenarios for the stock as we move further into the second semester of the year.

67% of all retail investor accounts lose money when trading CFDs with this provider.

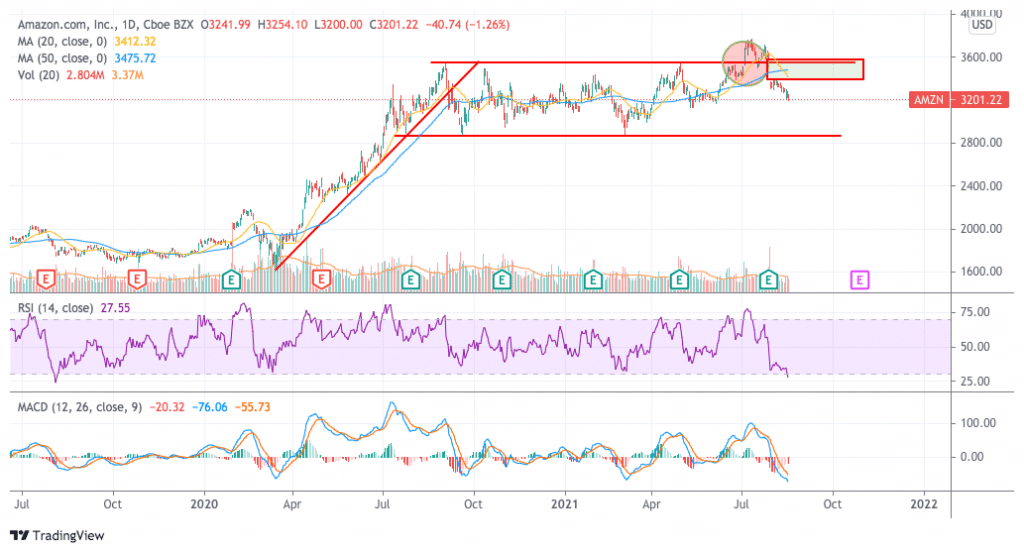

Amazon Stock – Technical Analysis

The technical picture for Amazon is not necessarily that ugly considering that the stock remains confined within the consolidation rectangle that emerged after last year’s pronounced pandemic uptrend.

A failed break of this rectangle took place back in July and effectively fooled buyers but then the stock retreated sharply after the release of this latest quarterly report.

Volumes back when the report was released were high, which can be expected, but they have also ticked higher in the past few losing sessions, which is more worrying as the stock has not even attempted to retest the upper bound of the gap that it left behind during this post-earnings downtick.

Momentum oscillators for Amazon are significantly bearish as the Relative Strength Index (RSI) has just reached its lowest levels since August 2019 while the MACD is posting its lowest reading since October 2018.

Even though these extremely bearish readings could be followed by a technical bounce, the outlook for Amazon stock is bearish based on what seems to be a full-blown trend reversal.

There are multiple support levels to watch if the downtrend persists in the following sessions including the $3,150 and $2,980 horizontal supports and the lower bound of the rectangle at $2,870 per share for total downside risk of 11%.

On the other hand, if the stock breaks below the rectangle, things would get uglier for Amazon shares as that would invalidate what has been until now a potential bull flag continuation pattern. Such a development would also significantly reduce the odds of recovering some of the lost territory on short notice.

Amazon Stock – Fundamental Analysis

Despite the company sharing a seemingly disappointing guidance for the third quarter of the year while also missing revenue estimates for the previous quarter, it is hard to deny that Amazon continues to be a high-growth company even if the pandemic tailwind fades.

In this regard, before the pandemic stroked, the company was growing its revenues at a pace of around 20% to 30% per year and even managed to push its top-line results 20% higher during the US-China trade war.

Meanwhile, gross profit margins have stood near the 40% level in the past few years while net margins have oscillated between 4% and 6%.

Therefore, despite this expected slowdown, the accelerated pace of the digital transformation – which was further fueled by the pandemic – could support the continuation of Amazon’s past positive performance even after the virus crisis is over.

At the moment, the company is trading at 57 times its forecasted earnings per share for the next twelve months while analysts are expecting a 26% average growth rate for the firm’s bottom-line results moving forward.

This results in a PEG multiple of 2 that seems quite attractive for a firm that has a small net debt, an elevated return on equity (ROE) of over 20%, a huge and fairly untapped global market, and a wide range of promising businesses that could further propel the company in the years to come.

Buy Stocks at Cedar FX, the World’s #1 trading platform!