Paycom Software Share Price Forecast August 2021 – Time to Buy PAYC?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

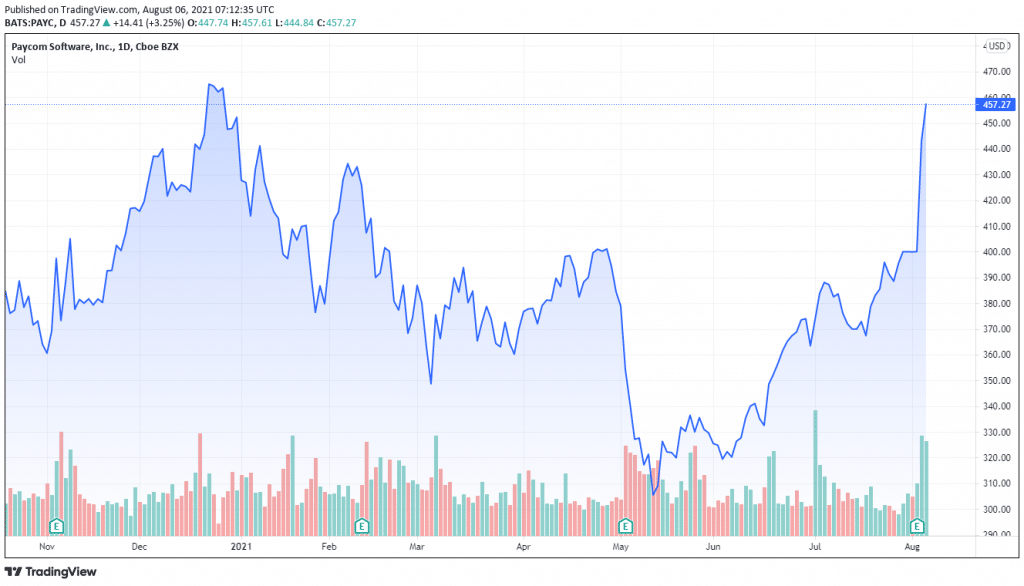

Shares of American online payroll and human resource technology provider Paycom Software (NYSE: PAYC) are in the green today after rising 3.25% to reach $457.27 as of 5th August, 4:04 pm GMT-4. The shares continue their good performance after Paycom released results for Q2 after Tuesday’s close.

Paycom Software – Technical Analysis

Paycom Software’s financial statement reveals a market cap of $26.48 billion and total assets worth $3.233 billion. Revenue for 2020 was at $841.43 million with a profit margin of 17.05%. This was an improvement from 2019’s revenue of $737.67 million. Revenues for the company increased by 33.3% year over year to reach $242 million for the quarter.

Oscillators such as Momentum (10)(71.73) and MACD Level (12, 26)(16.87) point towards buying. This is also indicated by almost all moving averages such as Exponential Moving Average (100)(372.60), Simple Moving Average (100)(365.27), Exponential Moving Average (200)(364.24) and Simple Moving Average (200)(384.79) which also point towards buying.

67% of all retail investor accounts lose money when trading CFDs with this provider.

Recent Developments

Paycom Software is widely regarded as the pioneer of fully online payroll providers in the United States with clients across all 50 states. It recently released a new software called Paycom Beti allowing employees to cut down on errors by using automation. Paycom released its Q2 results where earnings per share came in at $9.07, beating analyst’s expectations of $0.83. The company, which provides software programs for payroll management and human capital management has been boosted by the U.S. economy. The company’s demand is increasing as hiring and employment numbers increase.

To build a good rapport with customers and as part of its retention policy, each Paycom client is assigned a dedicated service specialist or providing personalised support. It bills clients on a monthly basis eliminating the need for long-term contracts. This makes it easier for clients to leave at any time if they wish. However, clients stock with the company for 10 years on average. Paycom’s customer retention rate for the last 3 years was 93%(2020), 93%(2019) and 92%(2018). This is a testament to the company’s ability to keep retention rates consistent throughout the Covid pandemic, despite facing hurdles such as double-digit unemployment rates and widespread business closures.

The company exited the quarter with cash and cash equivalents of $202.4 million, which is a slight decrease from the previous quarter’s $215.1 million. It generated $146.4 million in operating cash flow during the first half of 2021. The company’s management has projected adjusted EBITDA of $87 to $89 million. It has returned over 750% for shareholders in the past 5 years. It continues to perform well in the human capital market, outperforming its peers such as Paylocity and Oracle.

Should You Buy PAYC Shares?

Since going public in 2014, PAYC shares have always performed well. They are up almost 3000% during its time as a publicly traded company which dwarfed the S&P 500 index during the same period. The shares are currently trading at an expensive price-to-sales ratio of over 2, which can be a concern for current investors of the company. However, the shares are worth adding to your portfolio if the company continues to keep up its impressive 33% revenue growth over the next several years. According to figures from the U.S. Census Bureau, Pyacome serves 13% of its total market opportunity or 31000 clients. However, these figures may have been modified in the past 2 years due to the coronavirus pandemic. Investors should thus consider this crucial factor before they pick up PAYC shares.

Buy Paycom Software Shares at CedarFX, the World’s #1 trading platform!