EasyJet Stock Up 4% This Month – Time to Buy EZJ Stock?

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

The price of EasyJet stock has recovered in July after going down steadily in June, with the share price already delivering a 4% gain for investors since the month started.

Some of these gains have been caused by the EU’s refusal to adopt a proposal brought up by Germany’s Chancellor Angela Merkel to impose travel restrictions on passengers from the UK and other countries that have been affected by the Delta variant of the virus.

Meanwhile, the price of EZJ stock is moving higher for a second day, gaining 1.6% so far during today’s session at 931p per share.

This two-day uptick in EasyJet stock might have been supported by an announcement made by British authorities this morning that would facilitate traveling conditions for passengers going to the UK as the transport minister of the country stated that the government plans to eliminate its quarantine protocols for certain non-vaccinated arrivals in the following weeks.

Could this announcement result in EasyJet stock possibly surging to new post-pandemic highs? The technical setup of the stock suggests that such a scenario is fairly possible.

67% of all retail investor accounts lose money when trading CFDs with this provider.

EasyJet stock – technical analysis

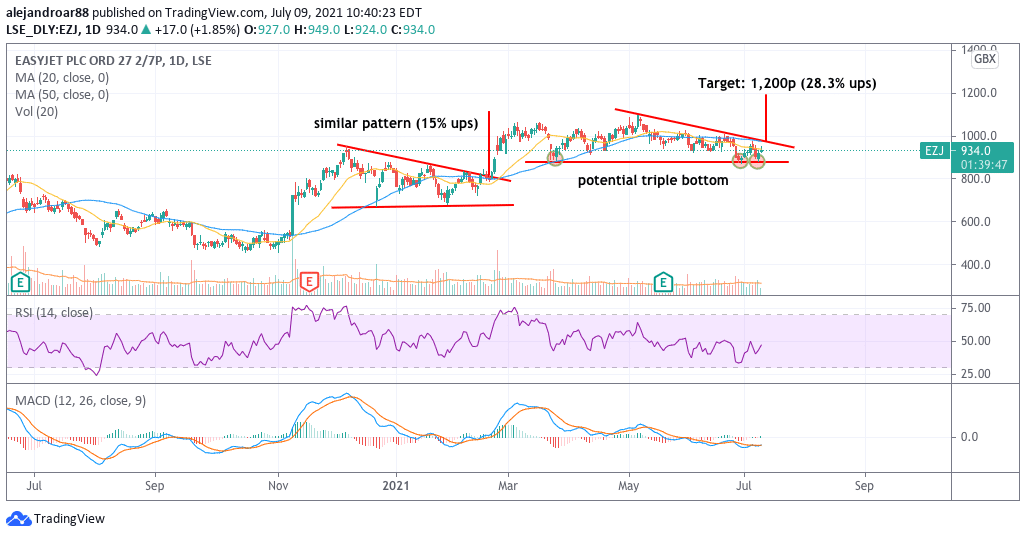

The price action seen by EasyJet stock in the past four months or so has resulted in the formation of a descending triangle – a typically bearish pattern that has led to bullish breakouts for EasyJet in the past.

As the chart shows, a similar pattern for EasyJet resolved to the upside this year, resulting in a 15% upside for those who traded the breakout.

This latest setup has been formed as a result of multiple tags of the 875p support level along with a series of lower highs for the stock. The latest tag of this support was accompanied by above-average trading volumes – which is often an indication of the importance of the threshold for market participants.

Based on the pattern’s previous bullish breakout, if the price surges past the 1,000p psychological resistance, chances are that EasyJet shares could move to the 1,200p level in the following weeks for a 20% upside potential.

This bullish outlook would be further strengthened if the RSI moves above the 55 level while it would also be positive to see the MACD moving above the signal line shortly after the breakout.

EasyJet stock – fundamental analysis

According to EasyJet’s latest interim report covering the six months ended on 31 March this year, the company said it expects to fly at 15% of its 2019 capacity during the third quarter of this year while the firm expects a surge in operating expenses during this period as it will be bringing back a portion of its crew to respond to an expected surge in demand during the fourth quarter of the year.

By the end of March, total revenues landed at £240 million, down 90% compared to the same period a year ago, during the worst days of the pandemic, while pre-tax losses landed at £645 million – nearly twice as much what the firm lost during the first half of its 2020 fiscal year.

The company reported a weekly cash burn of £39 million that may continue as-is for what remains of the year while its net debt stood at £2 billion on total liquidity of £5 billion.

Before the pandemic stroked, EasyJet sales grew from £4.7 billion in 2016 to £6.4 billion by the end of 2019 at a compounded annual growth rate of 10.8%. During that same period, net profits fell from £437 million to £349 million as a result of a sustained decline in operating margins.

Based on analysts’ estimates compiled by Koyfin, sales might not go back near the firm’s pre-pandemic levels until 2023 at least. Meanwhile, higher interest rates resulting from EasyJet’s now larger debt burden could depress the airline’s results even if it manages to push its sales near to where they were before the pandemic. In this scenario, bottom-line results could possibly land at around £100 million in 2023.

At a market capitalization of £4.26 billion, EasyJet appears to be trading at 43 times its 2023 forecasted bottom-line profitability. That ratio is fairly high for a company whose net profits could be severely affected by higher interest expenses resulting from its now elevated long-term debt levels while the firm still faces many important risks moving forward.

That said, EasyJet’s management has announced a cost savings program that could cut the firm’s operating expenses drastically this year. If the company manages to maintain higher levels of operating efficiency even once the pandemic is over, chances are that its bottom-line results could move above this estimate. However, investors must assess the likelihood of this scenario to determine if the current valuation is attractive based on that premise.

Buy Stocks at eToro, the World’s #1 trading platform!