Four Reasons for Digital Media Industry Growth

Please note that we are not authorised to provide any investment advice. The content on this page is for information purposes only.

The digital advertising ecosystem has evolved in mature markets around the world at an accelerated pace over the last 18 months, both in terms of volume of digital ad spend, as well as complexity of the value chain. Let’s face it, the mature markets have exploded.

There are two proof points to back up this statement.

The digital advertising ecosystem has evolved in mature markets around the world at an accelerated pace over the last 18 months, both in terms of volume of digital ad spend, as well as complexity of the value chain. Let’s face it, the mature markets have exploded.

There are two proof points to back up this statement.

First is the continuing increase in digital ad spend. In 2010, total digital advertising in the US increased 15 percent over the previous year. The display advertising component grew even faster at 24 percent year on year.

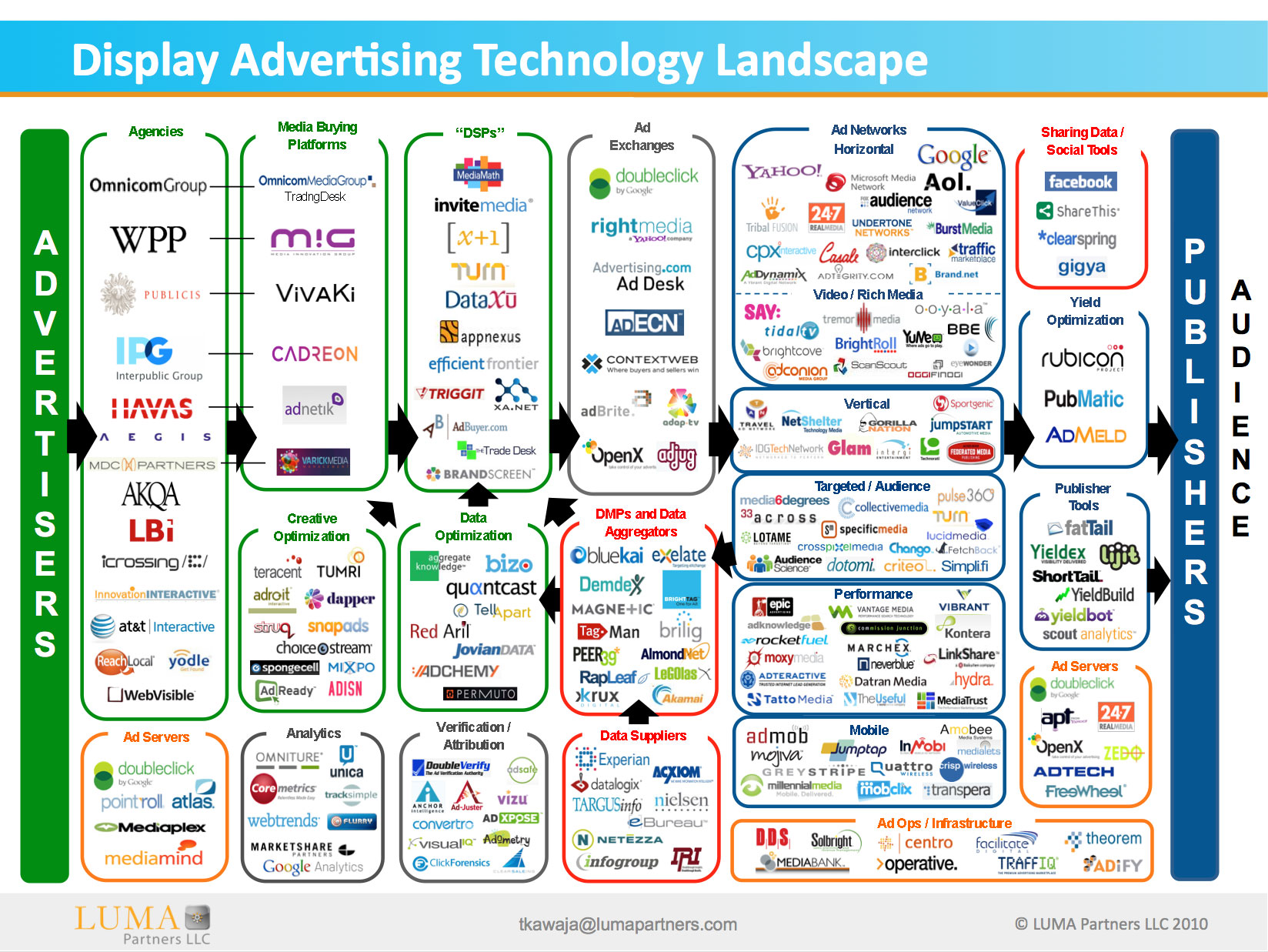

The second is illustrated in this Luma Partners infographic, a well known slide, but still highly relevant. As you will see, it is quite different from the much simpler publisher/ad network/advertiser OR advertiser/agency/search engine value chains of yore.

Source: Luma

What has led to this expansion and increase in complexity?

- The first reason is the disparity between how much time people spend with digital media and how much advertisers spend on digital. This factor is not new and has been influencing digital ad growth for a long time. However, recently it seems the shift is accelerating. Why?

- We believe it has a lot to do with emerging ecosystems of tradable advertising inventory. Trading in units of digital media exposure – be it clicks, impressions, or seconds of video viewing – has changed the world of digital advertising the same way financial trading floors – which used to be full of shouting traders – evolved into massive electronic trading platforms. This technology revolution changed the financial markets, bringing about massive liquidity and sometimes overwhelming complexity, and it is now happening to the advertising industry.

This change came about thanks to the following advances:

- Social media and increasingly, mobile social media. Both provide a wealth of data points that allow the advertising ecosystem to differentiate one impression from another.

- Real time bidding – provides infrastructure to publishers who want to have each impression priced separately based on its merits – as opposed to a day’s worth of impressions or a batch of thousands of impressions which became the industry standard.

- Ecommerce at scale – while it has been around for ages, it is only now that online sales have become a strategic sales channel for many industries. This has led to interest in previously obscure topics, including: cost per acquisition; programmatic media buying; algo optimization; and so on.

Include the digital advertising revolution with these three elements, and we have four major forces driving rapid change in the world’s mature markets. There are other technological “flares” that are relevant of course, but these are the four drivers increasing the complexity of mature markets by several degrees of magnitude.

Will this surge of volume and complexity impact Asia? Yes!

- Just as in the mature markets, agencies faced with increased complexity need 3rd party platforms – DSPs for starters.

- Demand from DSPs will drive development of other pieces, be it ad serving infrastructure or data providers.

- In Asia, where overall ad spend shift to digital is still in its infancy, changes will be faster and more sweeping. We believe it will form a cleaner, less fragmented, and more efficient ecosystem than the mature markets have formed through trial and error.

We believe it’s time to ask how will all that complexity run 90 per cent of the online world? AND how will it impact Asia, which only gets US$4-5 billion (excl. Japan) of the total global advertising spend, which currently stands at US$50 billion?

Two important questions to consider when Asia makes up nearly 60 percent of the world’s population.

This is how we see it:

- Because of the increased complexity, we expect that agencies will no longer “do” digital media planning and buying manually, as many in Asia continue to do today. Agencies rarely have the core competencies required to build scalable technology platforms, therefore we believe it is time for agencies to adopt some of the newer 3rd party platform.s

- The centrepiece of this 3rd party message is ad exchanges (RTB.) The most spoken about 3rd party solution is demand side platforms (DSPs,) or copy from Ad Exchangers. As a comparison, if you’re on NASDAQ you need a broker, and that is what a DSP is for digital media advertising. This is the technology that made NASDAQ possible, and this is what DSPs are.

- However, DSPs are not the ultimate and only solution – you need many other things to succeed – this includes data, context, delivery, operations, algorithms and integration. All of these aspects are appearing in Asia because advertisers are now demanding tradable inventory. The movement away from buying advertising in bulk/by inventory is happening.

- Once publishers have a critical mass of tools to manage inventory, data, and yields, we expect a virtuous cycle of supply and demand. RTB will account for an ever greater share of transactions, growing from a low single digit percentage to account for the majority of inventory traded in Asia.

Our goal is to simplify this complicated space by making it easier to use all the various pieces with one integrated platform.

Story from ADZ

ADZ is the digital media management platform of choice across Asia Pacific and the world.