Diverging Global Monetary Policies Plod On

The euro is trading at its lowest level against the Norwegian krone since August 2015. The euro is near its best levels against the Swedish krona in nearly as long.

The euro is trading at its lowest level against the Norwegian krone since August 2015. The euro is near its best levels against the Swedish krona in nearly as long.

The Federal Reserve decided to leave its target interest rate unchanged at a range of 0.25 percent to 0.5 percent while suggesting a hike later in the year was very likely.

Much of what the Bank of Japan announced today had been largely leaked. While there was a sizeable response in the asset markets, the dollar’s knee-jerk gains against the yen were quickly unwound.

The BOJ lifted its self-imposed restrictions on its asset purchases and shifted the focus of policy from the monetary base to the yield curve. It is not clear that this shift increases the chances of the BOJ reaching its inflation target.

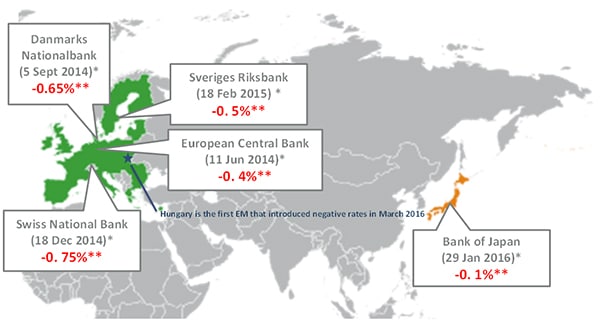

The ultra-low and negative interest rate environment in advanced economies and its implications for the rest of the world are currently among the top concerns of financial market participants and policy makers worldwide. Mark Carney, the governor of the Bank of England, recently said the low interest rate equilibrium1 is one of the challenges in which the global economy risks becoming trapped.

Tomorrow’s Bank of Japan and Federal Reserve meetings are serving to dampen activity in the foreign exchange market. The US dollar is little changed against the euro, yen, and sterling. The Antipodeans are firm.

The market has not changed its mind. Following Brainard’s comments yesterday the market had downgraded the chances, which were already modest, of a Fed hike next week. The September Fed funds futures is unchanged on the day. The implied yield of 41 bp matches the 50-day moving average.

Our approach to Fed-watching is clear: Among the cacophony of voices, the Troika of Fed leadership, Yellen, Fischer and Dudley provide the clearest signal. They are most often on message, and their comments have been the best indications of policy.

Remember at the end of last summer; Dudley said a rate hike was less compelling. This foretold the lack of hike last September. Earlier this year, as several regional presidents were talking up a rate hike, Yellen pushed against it.

The shaving of 2017 and 2018 growth forecasts, recognition of continued downside risks did not prompt the ECB to adjust monetary policy. Rates were left unchanged, as widely expected. The ECB also refrained from extending the asset purchases. This is somewhat disappointing. It was the only action that investors were discussing as a possibility. Bond yields appear to be backing up in response.

The last two weeks have been about the US. First, it was Jackson Hole. The leadership of the Federal Reserve, Yellen, Dudley and Fischer sang from the same songbook. They all signaled that the time was approaching to take another step in the normalization of monetary policy, without specifying precisely when.

Then it was the US employment report, which Fischer had specifically identified as important.

The world changed after the financial crisis in 2008. What lessons can we draw on the role of central banks since then?

There are at least four lessons we have learned.